Co-founder of Owned Outcomes Krupa Srinivas explores the value of fear in an entrepreneur’s journey as she describes partnering with a US healthcare intermediary to solve the problem of cataloguing hospital supplies. The US hospital supply chain is one of the largest supply chains in need of an overhaul. Market participants struggle with the lack of standardization, interoperability and transparency on quantities and prices of devices and supplies they purchase. Without industry-wide master unique identifiers for medical-surgical (med-surg) items, hospitals cannot easily compare products by their attributes to identify cost-savings opportunities, or map product selection to the best patient outcomes. In other words, an Amazon.com for hospital supply products is needed. The typical hospital spends about 30% of its annual budget on four to seven million items ranging from gloves and catheters to robotic surgery systems, totaling a staggering US$50 to US$250 million. Ordering is decentralized, based on personal preferences in both products and vendors, and at variable prices without strong ties to clinical outcomes. In 2015, one of the largest healthcare intermediaries in the country presented us these challenges. The organization asked our team of data scientists and engineers to build the most comprehensive med-surg catalog the healthcare industry had ever seen. This challenge spelled fear and opportunity in equal parts. We didn’t know the domainWhile we take pride in writing algorithms and building models to uncover the truth in healthcare data, we did not comprehend supply chains. We had to quickly understand the nuances in manufacturers’ product characterization, as well as how each purchaser (hospital) translated that into its own ordering systems. To build intuition, we turned to human experts. Observing and interviewing, we learned how to categorize a product, how to assign attributes to that product, and how to find values for those attributes. For instance, SKU #L122UV from Bausch+Lomb was categorized as Intraocular Lens (also called “IOL,” one of the test categories our customer assigned us) and had the following attributes: Optic Shape, Optic Material, Haptic Material, Pieces, Optic Diameter, Overall Diameter, Power, Haptic Design, A-Constant, AC Depth and Haptic Angle. We used this type of expert knowledge to power our semantic engines. LESSON: Watch an expert solve a problem before you build a machine to attempt it. Other people had struggled on this journeyIncumbent human processes were cumbersome, laborious, costly, slow and demoralizing. Having worse odds than a coin toss, the results were often obsolete before they could be compiled. New product introductions, product repackaging, rebranding, bundling and misaligned incentives were to blame. We started with the easiest problem that technology could attempt to solve. We wrote up a small list of words related to IOL: eye, ocular, lens, optic, power, etc., and had our scripts collate vocabulary (bag of words) from published literature. In a matter of hours, we had programmatically parsed through 1.1 million published articles, isolated around 2,500 of those that were related to IOL, generated about 1,200 attributes and identified roughly 3,300 possible values for them. Turning our attention then to the process issues, we whittled down to a manageable number of attributes (<25). Finally, we used human intelligence as the adjudication engine. LESSON: Technology solves silicon-intensive problems and humans solve judgment-intensive ones. Tight timeline, undefined goalsOur partner assigned a 60-day clock, provided 3TB of data spanning multiple years to build our proof of concept and asked us to do our best—and then wished us luck. Unsure of the bar for acceptance, we dove in to the data to discover that it contained over 20,000 items and unstructured text descriptions from thousands of hospitals. Escalating heart rates, sleep deprived eyes and much anxiety later, we delivered our first category 45 days later. Our attribution rate of 91% was a roaring success—we’d created a scalable technological solution in the process! LESSON: When solving large-scale problems, chase the art of the possible instead of settling for a pre-agreed target.

Ultimately, a little bit of fear breeds innovationWe love placing technology in service of tough problems. We celebrate the scrappiness, grit and risk tolerance. It turns our fears and applies our energy into building quick and iterating even quicker. Dreaming gets us started, creativity gets us excited, fear keeps us humble and relentless iteration gets us to the finish line.

The post How a Little Bit of Fear Breeds Innovation appeared first on Octane Blog – The official blog of the Entrepreneurs' Organization. via Octane Blog – The official blog of the Entrepreneurs' Organization https://ift.tt/2OgJpoH

0 Comments

We’ve heard about high-profile millionaires and billionaires announcing they will not be leaving their fortunes to their children. Is it a matter of time before this becomes a mainstream trend?It’s unclear how this trend will play out but we know with confidence that parents want their children to be better off—and they don’t define “better off” in purely financial terms. According to a recent Merrill Lynch survey, the no. 1 answer to the question, “What’s most important to pass on to the next generation?” for people over 45 was “values and life lessons.” The answer “financial assets or real estate” came in last. In between were “instructions and wishes to be fulfilled” and “personal possessions of emotional value.” My experiences with my own clients—particularly those who own businesses—confirm this finding. If faced with the choice of being able to hand down either their money or their values, I have found that they’d choose the latter. You might be able to attribute this choice to hard lessons learned in running a business to earn a living, but, in the end, it bodes well for the next generation. More and more parents today recognize that inherited wealth can easily be mismanaged or squandered if decoupled from values, a purpose or a credo. How can parents go about cultivating values in their children—specifically ones that are important to the entire family?Children learn a lot about values through allowances, specifically an allowance that emphasizes spending, saving and sharing (i.e., charitable giving). Asking your child to allocate his or her allowance to these three priorities on a consistent basis reinforces important messages to children at an early age. Moreover, at the appropriate age—around 7 or 8—parents should consider holding a family meeting to ask their children directly what’s important to them. Not only can parents bridge the family’s values with beliefs or goals important to their children, but children develop greater buy-in for a family’s values because they had input. I’ve also found that the act of writing something down on paper is helpful. Once values are written down after they’ve been articulated, they become easier to recall, teach and practice. Parents can then look for creative ways to remind their family of their values on a consistent basis. For example, displaying the values in a picture frame; giving gifts that reinforce the values, etc.

What can we do to reinforce values early with kids?One of the most important things parents can do is lead by example and make sure children see them practicing the values. For example, if you emphasize charitable giving with your family, you might pool monies together in a Donor Advised Fund not only to support a charitable cause important to the family, but also be able to recommend grants. Similarly, parents should bring their children with them to their favorite nonprofits while they are at an early age to show them the importance of volunteering personal time to a cause. Here again, allowances have a role to play to transmit values. Not only do children form positive memories when they contribute voluntarily to a charitable cause, but in doing so, they feel like adults. What can be done as part of estate planning to prepare the next generation for inheriting wealth?One of the most simple, effective and cost-free actions is creating an ethical will. The values that shaped a family or fueled the growth of, say, a family business can become the basis for an ethical will. Often no more than one or two pages, an ethical will allows you to share your vision for your family for generations to come. It can also go a long way toward instilling the values you expect inheritors to live by while encouraging them to consider how they should contribute to their community and the world. Any additional advice you wish to share about family businesses?Many parents have difficulty talking about their own mortality with their children—business owners included. This might be because the rigors of the business cycle have created hard opinions in a business-owner about how his or her estate should be divided among children, especially if the business is multi-generational. In these cases, family meetings can reveal solutions. It is not uncommon nowadays for estate planning attorneys and wealth advisors to bring in a professional facilitator to manage and guide family meetings. In some of my client experiences, I’ve found that a neutral third party helped families by getting them to examine issues from multiple angles so they can make better decisions. I also believe the entrepreneurial ethic itself can play a crucial role in passing on values. Showing unconditional love and letting children learn hard lessons on their own are two of the most important things entrepreneurial parents—any parents, in fact—can do. This means being supportive of and sacrificing for children, but also setting clear boundaries, letting them make mistakes and not bailing them out if they run into financial troubles. The post Tips for Passing on Your Values to the Next Generation appeared first on Octane Blog – The official blog of the Entrepreneurs' Organization. via Octane Blog – The official blog of the Entrepreneurs' Organization https://ift.tt/2qfDKpp The benefits of sleep can’t be overstated. “Good sleep guarantees wellbeing and mental health,” according to a study published on US National Library of Medicine. Indeed, sleep disorders are a significant factor in heart disease, with regular sleep rhythms and schedules being more important than sleep duration for your health. Sleep problems are also linked to metabolic syndrome and, thus, obesity. A study published in the American College of Occupational and Environmental Medicine concludes that, “insomnia and disturbed sleep…are associated with decreased job performance and productivity.” Sleep education, then, is an obvious investment for employers who wish to maximize productivity and, potentially, boost their bottom line. Pass along these 12 tips for improving sleep quality.

The post The Case for Good Sleep Can’t Be Denied appeared first on Octane Blog – The official blog of the Entrepreneurs' Organization. via Octane Blog – The official blog of the Entrepreneurs' Organization https://ift.tt/2CIPuYP

Written for EO by Grant Polachek, the director of marketing at Inc. 500 company Squadhelp.com. Part of being an entrepreneur or small business owner is getting excited about your venture. You obsess over it to the point that most of your daydreams revolve around details of your business plan—which beers you’ll offer at your new pizza place or the color of the walls in your designer boutique. This love and attention are what breathe life into your idea. But your collection of thoughts may also feel nebulous, like they haven’t fully solidified. Maybe it’s because you’re having trouble sharing exactly what your idea is. When people ask what your business is all about, you flounder. You jump across your ideas and fail to accurately capture the precise scope of your venture. Then, you worry you embarrassed yourself and that people will not take you seriously. This is why it is vital that you learn to condense your ideas into one simple value proposition. This succinct statement will help you focus your ideas and distill your business to its basic elements, which will later help you find the perfect name for your business. Brainstorming business name ideas is all about funneling your ideas down to the basics, and creating a value proposition can help you bridge your big ideas to their most condensed form—your business name. In this article, you will learn how to craft a strong value proposition and why having one is so important when it comes to sharing your ideas and brainstorming the perfect business name.How to Craft a Value PropositionYour value proposition, which in this case conveys the core of your business, is synonymous with your unique selling proposition, your business summary, your positioning statement, or even your mission. While we understand that these are actually slightly different concepts, this statement provides condensed direction. It should inform people what unique benefit your provide to your customers. It can refered to it as your elevator pitch. You are probably familiar with Domino’s Pizza: “Hot, fresh pizza delivered to your door in 30 minutes or less or it’s free.” Just like this, your sentence should be concise and descriptive while illustrating what makes your business stand out. To form a strong value proposition quickly, you can follow this basic formula: [Great Business Name] helps [audience] [core benefits]. Coming up with a statement like this will also help you grasp exactly what you aim to do. It condenses your long-winded idea into quick, digestible information. Why Bother With a Value Proposition?When setting forth with a new business idea, you will more likely be taken seriously and be seen as confident in your plan if you can succinctly state what you’re doing. For instance, it may be that your dream is to open a bookstore that showcases local publications as well as small press, and also includes a hip wine bar. Your bookstore is going to be a hub for your city’s creatives, a place where local artists congregate and exchange ideas. The wine bar offers casual service and a cozy, inviting environment. Your space caters to people who want to stay a while and connect with like-minded individuals to create community. Now let’s say you’ve been thinking all day about the variety of events you will host—from open mic nights to poetry workshops and events featuring local musician—when you’re asked by a stranger what your new business is all about. You rake your brain for a response that does not make your business sound like a waste of time, but you realize you haven’t replied. Because you don’t know how to accurately sum up your idea, you blurt out, “Well, I’m thinking about opening a bookstore.” In an instant, you’ve undervalued and trivialized the unique idea you have been mulling over for months, perhaps years. (And you’ve likely lost a potential customer.) Investing time and effort into defining your idea and what you’re all about in a way others can easily understand, a way that points out the benefits of your idea. Put pen to paper or finger tips to keyboard and challenge yourself to sum up your business effectively, in as few words as possible. But How Will This Help Me Name My Business?Writing your value proposition forces you define what your venture offers customers and how you plan to impact their lives. When naming, these are also things you should consider. Slowly whittling your idea down to its core will help you focus on the fundamental aspects of your brand. These core aspects are what your name should illustrate. Distilling your big idea down to a basic sentence may be hard to wrap your head around. There are so many unique facets to your business, you might be thinking. How could you possibly simplify it? One proven approach to naming is all about condensing your ideas. This not only helps you succinctly communicate your purpose, but also puts you in the right frame of mind to come up with a strong business name. A value proposition is a perfect jumping-off point to reaching the services and values that your business name must reflect. Let Your Value Proposition Guide YouDoes your business name even impact the success of your venture? In fact, it does. A great name will concretely boost your business, so taking the time to be thorough in your naming process will help you business flourish. Condensing your business idea into a simple statement can help you give others a solid grasp of what you’re doing. It is also an important step in the naming process. As you brainstorm business name ideas, your value proposition can provide direction and focus. Grant Polchek is the director of marketing at Squadhelp.com, the world’s no. 1 naming platform, with nearly 20,000 customers—from the smallest startups across the globe to the largest corporations including Nestle, Philips, Hilton, Pepsi, and AutoNation. Get inspired by exploring these winning brand name ideas. The post Proven Strategies for Brainstorming Business Names appeared first on Octane Blog – The official blog of the Entrepreneurs' Organization. via Octane Blog – The official blog of the Entrepreneurs' Organization https://ift.tt/2Sf6mMm

Fear of success. Self sabotage. Imposter syndrome. In the last 14 years of running my business, I have gone through cycles of all of the above. “Was it really me? Is it a fluke? Maybe it is a one off?” to “Maybe I cannot do it. What would people think about me?” So, I am so happy to have met Jeff Hoffman and heard his personal story. Jeff Hoffman is a successful serial entrepreneur who has co-founded many billion-dollar businesses such as priceline.com and ubid.com After a sale of one his companies, he went out for dinner with his friends. He wanted to celebrate with them and when the bill came, he decided to buy them dinner. He was shocked when they were actually upset at his gesture. They thought that he was trying to show off. The next time he went for dinner with the group, he was determined not to make the same mistake. So he asked what he should pay for his share, and they said, “Don’t worry, we will calculate to the exact cent, we don’t want to owe you anything!” It seemed that he couldn’t win. He grew upset as his success seemed to make his friends dislike him. That same night, he watched the news and saw women crying because the shelter they lived in was being shut down. The organization was running out of money to pay rent for the facility. And there was his answer. Then and there, he decided to anonymously donate a large sum of money to the shelter. His donation provided enough money to let them pay off their debt, keep the women and children securely housed and also create childcare facilities so that mothers could go to work. The next day, the women from the women shelter were on the news again. They were still crying, but this time, with tears of joy. Jeff realized that his hard work, his perseverance and his success had allowed him to help the women’s shelter. To them, his money was a miracle! He no longer felt badly about being successful because he could help less fortunate people with his hard-earned money. His story is a timely reminder for me that, as entrepreneurs, as change makers, as professionals, our success and accomplishments can have a much greater impact beyond ourselves. And it is our honor, privilege and responsibility to continue to work hard, persevere, do good and make a difference in the communities that we live in. Remember: your success is someone else’s miracle. The post Remember: Your Success Is Someone Else’s Miracle appeared first on Octane Blog – The official blog of the Entrepreneurs' Organization. via Octane Blog – The official blog of the Entrepreneurs' Organization https://ift.tt/2OCp8z7

Written by EO Germany member and CEO Feliks Eyser. A version of this article first appeared on Feliks’ Medium blog. Building an amazing company requires more than vision. You’ve heard the saying that every success story is 1% inspiration and 99% perspiration. You have to sweat and execute! Many people have good ideas, but few can execute and build a great company around it. It’s in the execution that a great chief operating officer (COO) comes in very useful! Why hire a COO?My strengths as chief executive officer (CEO) of RegioHelden were typical founder qualities: I was good at designing an MVP, persuading customers and employees, raising money and defining an overall vision and strategy. Some of my greatest assets were qualities like willpower, curiosity, creativity and impatience. These qualities got me quite far, but it took me some years to realize that those same assets could be liabilities when it came to building and managing an organization. I remember a situation where an early human resources manager quit after a few months and told me one of her reasons for leaving was she didn’t receive any management from me. Oops … I learned the hard way that starting a company and managing one require a different set of skills.

I might have been good at setting directions, recruiting and motivating the team, which were all important things, but I basically sucked at the managerial role. What does a COO actually do?To define these roles, I consider the Visionary and the Integrator. The Visionary focuses more on driving innovation, creating ideas and assessing the market. The Integrator tends to work on building the organization and maintaining business harmony. A good COO/Integrator defines systems and processes, manages staff, and ensures stability. Often the CEO role is focused externally (market, customers and investors) while the COO role is focused more inward (employees, organization design, processes and systems).

At RegioHelden my COO and I would sometimes distinguish our roles as “foreign minister” and “minister of the interior.” There may be certain organizations where one person can fill both the CEO and COO roles, but more often I see that splitting the roles between two persons with different skillsets is much more efficient--especially in scale-mode. When is the best time to hire a COO?As early as possible. I hired my first COO three years after I launched. That was about a half year after we raised the first million in VC. In retrospect, I should have filled the position earlier. Probably even during year one. The main reason? It’s hard to implement systems and processes in a rapidly growing company. Plus, maybe my HR manager would not have quit so quickly!

Think of it as building an engine while the car is running. The faster you get, the harder it will get to build up and fix things. So try to lay out a strong foundation of systems and processes before you put the pedal to the metal.

Striking a balance between growing quickly and building a solid foundation is always a challenge. But believe me, it’s worse to have a weak foundation and have the engine overheat than to grow a little slower but with a strong core. The 4 magical steps that will produce your next killer COOThe processes I used to hire our first COO in 2012 and the second one in 2018 were basically the same and are strongly inspired by Topgrading as well as the Who Method. Of course, the methodology is not limited to COO positions; I recommend a structured process like this for every position. The process boils down to these steps:

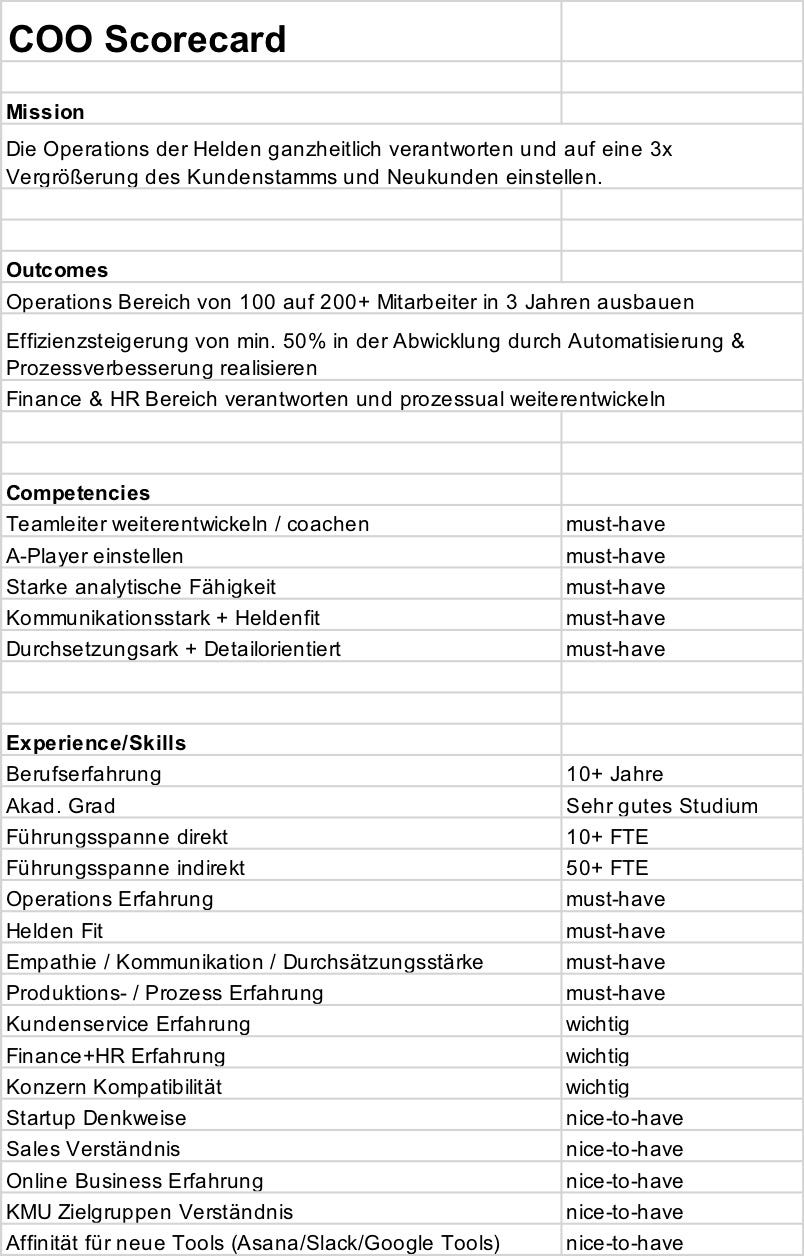

1. Define a scorecard and job descriptionThis planning phase is the most underrated step. A lot of first-time founders just throw together a job description without thinking much about the scope of the role. Big mistake.  Above is the scorecard for our company’s COO opening in 2018 (sorry for the German!). The scorecard includes the mission of the role, expected outcomes as well as competencies, experiences and skills that the candidate needs. Having such a scorecard has many advantages:

We then created a public job description based on the scorecard. That was pretty straightforward. 2. Fill the funnel to the maximumAt the top of the funnel, it’s just a numbers game: The more applications, the better. A lack of alternatives is never a good reason to hire a candidate. So focusing energy and some investment will create a big funnel and ultimately pay off. A lack of alternatives is never a good reason to hire a candidate. We used the following methods to generate applications:

These actions combined resulted in more than 250 applications in a timeframe of 6 to 8 weeks—pretty good for such a specialized role in a not-so-common city (Stuttgart). 3. Select with structured phone and personal interviewsFor the incoming applications we used the scorecard to measure candidates against the criteria in structured job interviews. To keep the process efficient my HR manager would first conduct a 30-minute phone interview. Then, the good candidates came to me. I would either do phone interview or invite the candidate to our office for an in-person interview. After the first interviews, we’d enter numbers on the scorecard to grade applicants for competencies and experience. The goal here is to bring structure and objectivity into a traditionally emotional and biased part of the process. We used the same scorecard for both the phone interviews as well as in-person interviews but would reduce the number of questions in the phone calls. If you want to learn more about how to conduct structured job interviews (and, if you don’t know what that means, you should!), I recommend the books Topgrading and Who. 4. Testdrive and check references with the teamFor the final five to six candidates, we complete testdrive days. We send each person the same three assignments to prepare and present in our office in front of the C-level team as well as their future direct reports (six to 10 people). The workshop meetings took 60 to 90 minutes, and included the candidate’s presentations as well as a question and answer session. Afterward, the candidates would sometimes talk with their potential reports or we would all go to lunch together. Including the direct reports is very important for several reasons:

In the first COO search, we also allowed board members to interview the final candidate. After the testdrives and final interviews we completed checks on references that the candidate provided as well as contacts from our network who have worked with the candidate. When we found the perfect candidate the rest was just negotiation of their compensation package and legal paperwork. Usually at this point the candidates were pretty committed. In both cases, we got very lucky and we were able to sign the candidates in under 4 months. As a rule of thumb, I would allow six to 12 months from the start of the recruiting process until the candidate actually starts. That includes the recruiting process itself as well as the cancelation period of the candidate with their old employer (in our case, usually three to six months or until end-of-quarter). To that, I add another six to 12 months for the new COO to be properly on-boarded and trained before he or she is fully effective. (Two more reasons to start the recruiting early. Use this methodology to hire a killer COO, and drive your startup to the next level! The post 4 Steps to Hiring a Rock Star COO (Plus, Why You Need a COO!) appeared first on Octane Blog – The official blog of the Entrepreneurs' Organization. via Octane Blog – The official blog of the Entrepreneurs' Organization https://ift.tt/2NPB0IG

Here, we reveal seven practices that could be sabotaging your growth:

Starting at 12:00 a.m. GMT on 12 November, and continuing every day throughout the five-day week, EO 24/7 will unlock unparalleled learning with videos, podcasts and articles that focus on helping you with your entrepreneurial journey. Watch, learn and engage with leading entrepreneurs from the convenience of your computer screen beginning on 12 November. Unlock this learning experience for free--register today for EO 24/7. The post 7 Habits That Keep Women Stuck appeared first on Octane Blog – The official blog of the Entrepreneurs' Organization. via Octane Blog – The official blog of the Entrepreneurs' Organization https://ift.tt/2J2Bp9Z

Written for EO by Dave Pributsky, cofounder of 2920 Sleep One day, a hare was making fun of a tortoise for being so slow. “Do you ever get anywhere?” the hare asked with a mocking laugh. “Yes,” the tortoise replied, “and I’ll get there sooner than you think. I’ll run you a race and prove it.” No, this isn’t storytime for entrepreneurs. At some time in our lives, we’ve heard the tale of “The Tortoise and the Hare.” This classic fable teaches us that the race does not always go to the fastest. Rapid growth and market dominance might seem great in the business world, but they are not goals that every company—or every leader—should chase blindly. Sometimes it’s better to start slow and truly understand your market before shifting into rapid-growth mode. Lessons From the ThroneWhile we rightly celebrate the Amazons, Apples, and Googles of the world for their tremendous success, let’s not forget about the many promising companies that flew too close to the sun too quickly. Remember Pets.com? The online pet food and supply retailer raised hundreds of millions of dollars from investors before ultimately closing up shop because it ran out of money. Investors expected the dot-com startup to rapidly grow its customer base to generate revenue, but it ended up running things into the ground because of an overly aggressive approach. Need more proof that rapid growth isn’t all that it seems? Researchers found that many of the companies that appeared on the Inc. 5000—a list of the fastest-growing private companies in America—were not doing so well five to eight years after the accolade. In fact, two-thirds of those organizations had either shut down, become smaller over time, or been sold off. While meteoric success might seem like a dream scenario for founders and early-stage entrepreneurs, there are clearly some drawbacks. When Less Is MoreIn many cases, the healthiest path for a company might not be to “grow as fast as possible.” I have been fortunate to work at both small private firms and a classic Silicon Beach unicorn with a successful billion-dollar IPO. I’ve been lucky to view success and failure on several different scales. What I’ve learned is that a growth-at-all-costs mindset might not always be the best approach. A successful business leader needs to be aware of the cost of growth against company culture, the ability to sustain that growth, and the consequences growth might have on the executive team. Working with this type of leader is like having Phil Jackson or John Wooden as the coach. They know when to push, and they know when it’s time to ease up. I believe this wisdom works as well in large-scale business as it does on the basketball court—or in smaller businesses. A slow-but-smart growth strategy can outperform both rapid-growth and zero-growth approaches. Here are a few ways to lead your team to sensible (not just sensational) growth: 1. Set your priorities. We all wanted to enjoy more quality time with our families, spend time outdoors and feel good about how we treated our business partners and customers. That meant we had to adjust some of our financial targets. For example, we made a commitment to allocate 1 percent of our revenues to environmental causes via 1 % for the Planet. When your goals and priorities are explicit, you can make more fulfilling choices about how you spend your time and money. 2. Align and communicate. One study found that 73 percent of employees who report working for a purpose-driven company are engaged. In other words, getting the right people to buy into the company’s strategies will benefit everyone involved. 3. Express your gratitude. There may come a time when you are ready to take over the world with your business. You might eventually be the king of your vertical, but you might not want to aim to get there overnight. With some careful planning and a little introspection, you can hopefully enjoy your journey without unnecessary growing pains. Dave Pributsky is the head of marketing strategy and business development at 2920 Sleep. This customer-centric online retailer provides high-quality products that improve sleep quality and overall health with minimal environmental impact. Dave founded 2920 Sleep with his business partner, Karim O’Driscoll. Dave has experience leading business and digital strategy with consumer brands such as TrueCar, USAA, AAA, American Express, and Consumer Reports. The post Slow Is Fast: Think Before Chasing Rapid Growth appeared first on Octane Blog – The official blog of the Entrepreneurs' Organization. via Octane Blog – The official blog of the Entrepreneurs' Organization https://ift.tt/2CjGrh8

Written for EO by Floyd DePalma, CEO of UX agency DePalma Studios. When I started DePalma Studios, my mission was to design and build applications that people love to use. Six years into my entrepreneurial journey, I had achieved the goal of being my own boss. It was satisfying on a personal level, but the business had plateaued around the three-year mark. It wasn’t growing how I envisioned. In search of a solution to grow my business, I decided to enroll in the Entrepreneur Organization’s Catalyst program taught by Michael Burcham. I’d heard great things about the class, and as a member of EO’s Nashville chapter, I could join at no cost. The topic for the first class was “A New Attitude,” and it started with the message, “if you’re not scaling up, you’re stalling out.” It was a real wakeup call for me. After the very first class, my entire perspective on what it meant to be an entrepreneur changed. So I bought in to everything Catalyst offered and the results speak for themselves: In 1 year we’ve added 30 new clients—a record year for the agency. Transitioning From a Founder to a LeaderThe goal of the Catalyst program is to make founders take a step back and honestly assess their current business. This helps them learn how to improve and reimagine what’s possible by developing greater discipline and focusing on fundamental business strategies. This is the central tenet behind transitioning from a founder to a leader. I began to think like a leader. And using what I learned in the Catalyst program, I focused on five core areas of my leadership style and the organization as a whole. #1 Organizational DevelopmentMy first move was to look at how I’d structured the organization and who I had on staff. I realized I needed to make some changes and additions to key management positions and our production team configuration. I started by filling the management gaps in our organization. I hired a creative director to lead our UX design department and an experienced engagement manager to lead our engineering department. Finally, we moved our production resources nearshore and offshore to increase scalability and profitability. #2 Design ThinkingThe principle of design thinking can be a powerful one if you have the right people in leadership positions. You need A-players who are self-starters to help you think about how to grow the business. This type of leadership team is capable of creating processes to execute against the strategy which, in turn, creates a cycle of innovation. Thanks to that approach, we now have:

#3 Process OptimizationBefore Catalyst, I didn’t have a single documented process. All the work was done on an ad-hoc basis. That means that it was done differently every time depending on who was doing it that day. You can’t grow a business that way. All of your core competencies must be process-driven so they can be optimized to enable the business to innovate and drive profitability. Now we have battle-tested processes that we continue to iterative and improve in the following areas:

#4 Financial ModelingOut of all the areas of focus, knowing my numbers and financial modeling is where I’ve done deepest dive. A year ago I was picking a revenue goal out of thin air. Now, I work my way backward into revenue using a model that focuses on bottom line pre-tax profit as the target instead of top line revenue, which is just a vanity KPI. Now, I have a trustworthy financial model for calculating the health of my business—and planning for its future. I now focus on the real fuel that drives the profitability: labor efficiency rate (LER). I track LER’s for everyone in the company: indirect labor, direct labor, contract labor. These numbers tell me the exact ROI in dollars and cents for every dollar spend. Using LER calculations, I’m now able to set my markup on services systematically to get the correct margins that I need for growth. #5 Strategic MindsetAll of the previous points illustrate how my thinking has changed to be more strategic. Instead of being reactive, I’m always in planning mode. I’m looking six months ahead of where the business is today and planning for upcoming quarters. With this new attitude my role as a strategic leader has become:

By thinking less like a founder and more like a leader, I’m now running a growing business instead of organization that’s standing still.

The post How I Went from Startup Founder to Leader of a Growing Business appeared first on Octane Blog – The official blog of the Entrepreneurs' Organization. via Octane Blog – The official blog of the Entrepreneurs' Organization https://ift.tt/2ONAks1

Written for EO by Michael Neidert, a writer and consultant. Finance is a common source of both challenges and opportunities for a growing company. What you are spending your money on and when you spend are often key indicators for an organization’s financial success or failure. When you’re thinking about sales, you may forget about setting a savings rate. When you’re thinking about saving money, you may miss out on places to continue spending. When you’re just trying to make it through the end of the month, you may lose focus on your long-term goals. Learn these foundational finance lessons now to set yourself up for success: |

AuthorWrite something about yourself. No need to be fancy, just an overview. Archives

November 2020

Categories |

Krupa Srinivas is the co-founder of Owned Outcomes, a software company that enables data-driven decision making for healthcare providers and payers as they seek financial sustainability alongside clinical outcomes in patient care. She is currently serving a governor-appointed position on the Information Technology Advisory Board for the State of Nevada. Krupa joined

Krupa Srinivas is the co-founder of Owned Outcomes, a software company that enables data-driven decision making for healthcare providers and payers as they seek financial sustainability alongside clinical outcomes in patient care. She is currently serving a governor-appointed position on the Information Technology Advisory Board for the State of Nevada. Krupa joined  The lessons learned through bootstrapping are important not only to entrepreneurs and their workforces, but to their children as well. Whether your kids will one day run the family business or you simply wish to pass on the values and work ethics that helped you succeed in starting and owning a business, devoting time to coaching your children can feel like its own challenge.

The lessons learned through bootstrapping are important not only to entrepreneurs and their workforces, but to their children as well. Whether your kids will one day run the family business or you simply wish to pass on the values and work ethics that helped you succeed in starting and owning a business, devoting time to coaching your children can feel like its own challenge.  If you are interested in creating a positive legacy, then you will want to

If you are interested in creating a positive legacy, then you will want to

Written by Violet Lim,

Written by Violet Lim,

Women’s leadership expert Sally Helgesen and leadership coach Marshall Goldsmith join forces to address the common and specific roadblocks women face in their pursuit of professional success in the book

Women’s leadership expert Sally Helgesen and leadership coach Marshall Goldsmith join forces to address the common and specific roadblocks women face in their pursuit of professional success in the book  Sally Helgesen and Marshall Goldsmith are among the world-class speakers at EO24/7, our exclusive annual virtual-learning event!

Sally Helgesen and Marshall Goldsmith are among the world-class speakers at EO24/7, our exclusive annual virtual-learning event!

Floyd DePalma is the Founder and CEO of DePalma Studios, a

Floyd DePalma is the Founder and CEO of DePalma Studios, a

Save wisely

Save wisely

RSS Feed

RSS Feed